The Case for Trump Accounts: A Debate

Every American deserves a stake in the economy.

Editor’s Note: This is the first of a two-part debate on the value of Trump Accounts. Michael Lind’s response here.

What’s the point of capitalism if people don’t have capital? An ownership society without owners? An American Dream without the assets—a home, an education, a retirement account—that make the dream possible?

That’s unfortunately the situation for too many Americans, especially younger ones, who face unprecedented headwinds in finding their footing in this economy. Federal Reserve data show that, among those living with kids under age 18, average financial or investable assets stand at $700 in the bottom 20%, $9,200 in the next 20%, and $38,300 in the middle quintile. And they’re especially left out of the stock market, which has seen remarkable growth over the last few decades: average holdings are $11 for the bottom 20%, $2,265 for the next 20%, and $13,502 for the middle 20%.

Enabling newborns to invest is naturally the best way to counter that—exactly the intention behind Trump Accounts, a new type of traditional IRA established at birth with a $1,000 federal deposit for over 14 million newborns between 2025 and 2028 (and open to all children under age 18 but without the $1,000 deposit). Trump Accounts (also known as 530A accounts for the section of the tax code in which they reside) were dropped into the One Big Beautiful Bill and signed into law on July 4 of last year, building on bipartisan support for the idea over the last few decades.

Three features aim to maximize the critical “start-up capital” young adults will need: the funds must be invested in a broad-based index fund like the S&P 500, no withdrawals are permitted prior to age 18, and a wide range of nonprofits and government entities are encouraged to contribute.

Given these features, balances could be substantial. A Milken Institute paper by Michael Piwowar and Robert Shapiro, using Monte Carlo simulations, reports that the initial $1,000—with no additional contributions—could become $8,308 in 20 years, $69,024 in 40 years, and $574,397 in 60 years. They also observe that matching the initial $1,000 could double these values, something a few dozen employers and the states of Texas and Oklahoma have pledged to do. Furthermore, starting at age 18, contributions from lower-income workers would qualify for the new federal Savers Match, which could boost retirement savings by as much as 50%.

Will Trump Accounts Increase Wealth Inequality? Probably, but…

Because Trump Accounts are universal—actress Hailee Steinfeld’s and NFL quarterback Josh Allen’s expected child is eligible for the $1,000 federal deposit along with every child born to the poorest parents in the U.S—and because rich families are far more likely to save the maximum $5,000 a year in the accounts, a common critique is that they are likely to increase near all-time high wealth inequality.

And that critique appears correct! But it doesn’t change the answer to what I believe is the more important question: Are lower-income and middle-class kids more likely to be better off with a Trump Account than without one? Yes! For that reason, Congress and the president did the right thing by enacting Trump Accounts into law.

First, and for the record: after leading a wealth inequality research center at the St. Louis Fed for over a decade, I believe wealth inequality is a serious problem—a barometer for a range of economic, social and political ills in the U.S that Congress and others must address.

Yet the many issues driving wealth inequality—e.g., radical reductions of taxation on higher-income and wealthy Americans; taxing wealth-derived income at preferential rates; massive pension and homeownership tax breaks whose value rises with income; the top 20% owning the overwhelming value of stocks; trade policy, deregulation, corporate tax cuts, the erosion of unions—won’t really change because a few million better-off kids get $1,000 at birth and their parents and others may sock away thousands more each year.

In fact, and more fundamentally, if a slight uptick in inequality is the price we pay for a universal policy—one that, therefore, includes millions of households with genuine needs to build wealth—then that’s well worth it. Universal policies, too, tend to be more enduring.

Why Lower- and Middle-Income Kids Would Benefit from a Trump Account

It’s far from clear, however, that better-off families would save in a Trump Account, given the wide array of investment products available to them and the better tax benefits and flexibility of those products. But Trump Accounts could mean a lot to lower- and middle-income kids—the vast majority of whom will see nothing from the so-called “great wealth transfer” from Boomers to their kids and grandkids.

In addition to giving youth some start-up capital in an economy conspiring against them, let me offer three additional reasons why Trump Accounts are likely to be good for lower- and middle-income kids—and thus good for our society and economy.

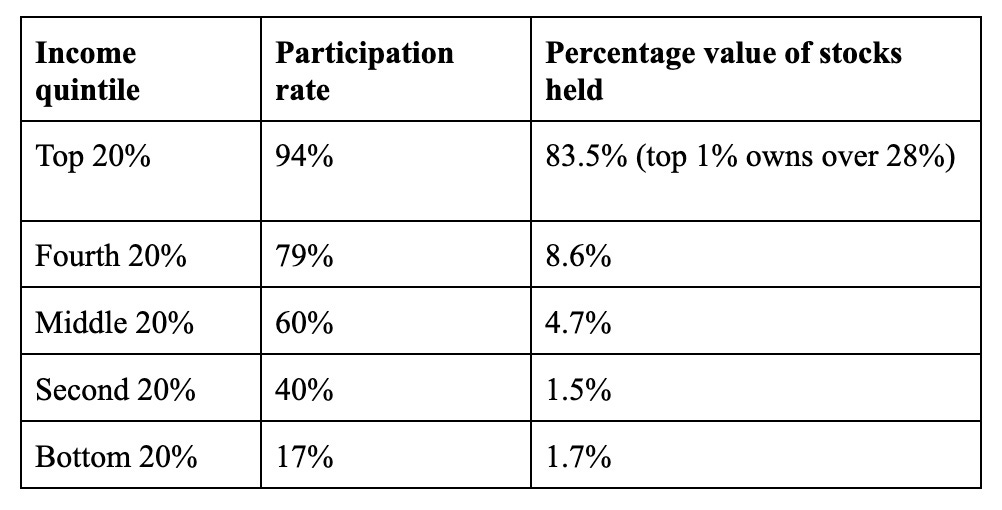

1. Exposure to the Stock Market. One of the most exciting features of Trump Accounts is that they open up stock ownership to the bottom half of the population, which holds only 2.5% of the nation’s wealth and an even lower 1% of corporate equities and mutual funds.

Unpacking that at the household level, Ana Kent, a former wealth inequality researcher at the St. Louis Fed, found using Federal Reserve data that while a significant portion of Americans have some participation in the stock market, the value of stocks held by the bottom four quintiles is quite low:

Source: Federal Reserve’s Survey of Consumer Finances (2022) and Kent’s calculations. Note: Direct and indirect stock holdings, including in retirement accounts.

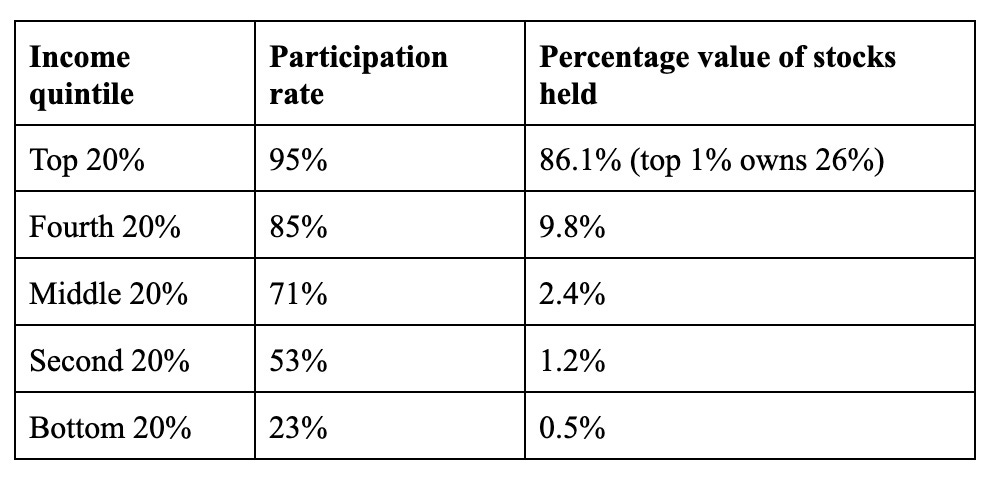

Kent further found that, looking just at households with kids under age 18, stock market participation rates are higher but holdings are even more concentrated at the top:

Source: Federal Reserve’s Survey of Consumer Finances (2022) and Kent’s calculations. Note: Direct and indirect stock holdings, including in retirement accounts. Income quintiles among households with kids under the age of 18.

Of course, enormous volatility in the stock market, combined with the S&P 500 being dominated by the so-called “Magnificent 7,” should give us pause in recommending it as a reliable savings vehicle. But the stock market has become one of the most steady routes to wealth creation in the U.S. over time. The S&P 500 has returned over 8% so far this year, about 17% in 2025, and about 10% over the last 30 years. And the best thing newborns have is time.

Moreover, we need new routes to wealth creation, especially for those lacking wealth from which to start. For decades, lower- and middle-class families have fairly reliably built wealth through homeownership and post-secondary education—but these assets are not necessarily wealth-building any longer.

A college degree, for example, as we documented at the St. Louis Fed, has had diminishing returns (especially wealth returns, compared to income returns) for younger generations, while other scholars have found that housing returns are becoming riskier and more cyclical, especially for black and Hispanic homeowners. Policymakers and others should address these declining college premiums—but why not let every American enjoy the more reliable gains from the stock market, what Invest America (which helped drive Trump Accounts into law) calls the “upside” of America?

And for those who, like me, care about reducing the racial wealth gap, we cannot ignore the stock market. As Ken-Hou Lin and Guillermo Dominguez found in 2023:

The contribution of stock-linked assets to the Black–White wealth gap has expanded in both absolute and relative terms, surpassing those of homeownership and business equity. Furthermore, a substantial disparity in financial wealth exists even for otherwise similar Black and White households. Although the disparity is larger among those with more economic resources, a gap remains among those with less. Lastly, our analysis shows that the combination of lower ownership levels and lower returns on financial wealth among Black households could account for a quarter of the Black–White wealth accumulation gap, net of differences in current net worth and household characteristics.

That is, to the surprise of many, Trump Accounts also hold the potential to narrow the racial wealth gap.

2. A Magnet for a Shared, Community Asset. Among the most unique (though admittedly complex) features of Trump Accounts is the explicit encouragement of multiple contributors in support of a child’s future. Post-tax (already taxed going in, tax-free coming out) contributions of up to $5,000 per year total may come from families and others.

And then there are three possible pre-tax (not taxed going in, taxed coming out) contributions: the federal $1,000 deposit; employer contributions up to $2,500 per employee per year (some 40 major corporations have already pledged support); and, the “general contributions,” which encourage 501(c)(3)s, philanthropists, cities, states, and Tribes to contribute unlimited though equal amounts in pre-defined geographical areas or for certain birth cohorts.

This third route is what Michael and Susan Dell used to target their unprecedented $6.25 billion contribution: $250 to 25 million children ages two to ten in zip codes with a median family income of $150,000 or below. Ray Dalio made a similar pledge for children in Connecticut, while Trump Account evangelist Brad Gerstner pledged to contribute to all children under age 5 in Indiana, his home state.

This wide range of contributors into one account reflects a powerful idea pioneered by University of Michigan scholar William Elliott III and NYC Kids RISE Founding Director Debra-Ellen Glickstein: that Trump Accounts are not just or even primarily personal savings accounts, but a shared, community-driven, wealth-building platform. As Elliott summarized his research for me in an e-mail:

Trump Accounts embed an institutional reservoir logic in federal law, treating children’s savings accounts (CSAs) as civic infrastructure rather than a private financial product. The account is built to capture flows from multiple streams—federal seeds, employers, philanthropies, community groups, and families—and, in doing so, to convert asset streams into social capital streams. Properly designed CSAs cultivate bonding ties within families and neighborhoods, bridging ties across communities, and linking ties to powerful institutions like city governments, banks, and major employers. NYC Kids RISE illustrates how this multi-stream, community-driven model both raises balances in low-wealth neighborhoods and marks children as shared objects of community investment, turning what looks like an individual account into a community account that builds social capital as well as wealth.

And not only should Trump Accounts not be viewed as primarily personal savings accounts: they should never be the basis for privatizing Social Security (or any social insurance program). As memorably observed by Invest America’s Matt Lira, Trump Accounts are about how kids start life, not how they end it.

3. A Future Orientation and Hope. A third and final compelling reason to support Trump Accounts is that, as research shows, they are poised to change thinking and behavior in positive ways—even if families do not save or save very little. It’s the presence of the asset in the household that generates these powerful “asset effects.”

Nearly two decades of experimental research from SEED OK—led by Michael Sherraden, the field’s intellectual pioneer and author of the seminal 1991 book Assets and the Poor—have demonstrated the effectiveness of at-birth Child Development Account (CDAs), precursors to Trump Accounts. SEED OK research led by Jin Huang found that CDAs:

Give parents new hope for their children’s future and may change how they interact with their children;

Help mothers maintain or increase their expectations;

Improve parent-child educational engagement;

Enhance college preparation for their children’s postsecondary education;

Reduce symptoms of depression reported by mothers, particularly disadvantaged ones; and

Improve children’s early social-emotional development, children’s hope, and adolescents’ behaviors, regardless of parental saving behavior.

Elliott also found that CDAs cultivate college-going or “college bound” identities and reduce “wilt,” or failing to transition to college despite having the desire and ability to go. A low- and moderate-income child who has school savings of $1 to $499 prior to reaching college age is over three times more likely to enroll in college and four times more likely to graduate from college than a child with no savings account.

Finally, it’s worth noting that these positive asset effects are likely to be further “supercharged” by the multiple investors in Trump Accounts described above. Imagine a child knowing that it’s not just their family who believes in them, but their government, their local bank, a local nonprofit, a big-name donor, their parents’ employer, and others.

Moving Forward

My enthusiasm around having investment accounts at birth in law—an idea I worked on for over two decades in and with Congress—is not unqualified. Like with most ideas that find their way into law, there’s much I would have done differently and will work diligently to see changed in the future. That sentiment is shared by a quiet, though growing and bipartisan, set of lawmakers on Capitol Hill.

First and foremost, every child should be automatically enrolled in a Trump Account, and the $1,000 should be automatically deposited for eligible newborns. All the benefits of Trump Accounts I just articulated mean nothing unless kids have accounts, as Sherraden and I have argued before. While an impressive six million-plus families have opted in already, that’s millions short of the number of newborns and children under 18 who are eligible.

We also need “progressive” deposits—additional deposits for kids in lower-wealth families, especially if we’d like to narrow racial and other wealth gaps and reduce the potentially inequality-enhancing effects of the accounts. Critically, once kids turn 18, we also have to ensure that any savings and withdrawals from Trump Accounts (which, officially, become a traditional IRA at age 18) do not impact eligibility for any means-tested public assistance program such as Medicaid, SSI, and student loans.

And, finally, the $1,000 federal deposit should be extended beyond 2028 so that Trump Accounts become a permanent part of the social contract for families with kids which, up until now, largely (though inadequately) focuses on income, cash, health, nutrition, and other support.

U.S. history is full of bold, new public policies becoming better over time, such as the 1944 Servicemen’s Readjustment Act, better known as the G.I. Bill, which also aimed to broaden asset ownership but started out excluding minorities and women. Trump Accounts also can and should improve over time. The long view is critical in this line of work—but, thankfully, we now have a great place to start.

| A guest post by

|

I have ongoing debates with people that are on my-side of the political fence that are determined to keep demanding that the system that supports them being high income and high wealth is fair enough and that the rest just don't work hard enough or make the right decisions, and that is why they are stuck in lower income and wealth.

While certainly there are plenty of lazy people prone to making bad life decisions, my peers of conservative libertarian economic thinking are fooling themselves that we have not gone far passed the time that we can claim we have a well-functioning democratic capitalist system. What we have today is a globalist corporatist system... maybe a global corporatocracy. It is powered by Wall Street, and it is focused almost exclusively on wealth creation for the top 10% from higher investment returns and higher corporate profit... and the expense of almost everything else.

We need massive new rules to stop the corporate consolidation that is killing competition and cutting out too many people from access to the real economy.

I think Trump Accounts are a good example of much that is wrong with our economy and our country: it’s a program that is unserious, nonsensical, mostly sloganeering, and where the benefits mostly accrue for many years primarily to the wealthy.

Sure, let’s have yet another vehicle to help people save money for the future. That’s fine. But that can be done – and mostly already existed before this latest law. The only new twist here is the government contribution. So let’s focus on that.

Here’s what it is: the federal government prints $1,000 in new money, which is inflationary, and adds it to the existing federal debt. For the rest of history, our children and grandchildren will pay interest to the rich people and governments who buy Treasury bonds to finance this debt.

That new debt is then handed out to a child, and sits for 18 years, further propping up the S&P 500 equity bubble that overwhelmingly benefits the top 25% of Americans (and distorts our economy). Wall St. bankers will generate fees for managing these Trump accounts for 18 years before a child can even touch it.

Then, 18 years from now, the account holder will turn 18, and have perhaps $7,000 in the account handed to them to do whatever they want with. (Of course, these are nominal dollars. Who knows what buying power will remain after inflation continues to do its dirty deed for the next 18 years.) The newly-minted 18 year-old can cash it out immediately by paying a 10% fine, using the remaining $6,300 to pay tuition, put towards the purchase of a car, create the next Tesla, or spend on DraftKings and vape products. There will be some wonderful conflicts in families as Uncle Sam hands a teenager $6,300 cash beyond his or her parents’ legal control.

The simple question that obliterates the Trump Account fantasy is this: if printing $15 billion in new debt over the first 10 years (one program estimate) and dropping it into the S&P 500 in $1,000 increments makes sense, why not print $150 billion – or $15 trillion – and drop it into the stock market?

To even ask the question is considered unkind – why be a killjoy?!?! Printing money today and sending the bill to future Americans is THE AMERICAN WAY!

But someone has to speak truth to nonsense. Printing money and stuffing it into the stock market does NOT generate wealth, even if no one has the cojones to admit it. But it sure helps the wealthy and rich keep the bubble bubbling.

A total scam. Conservatives should admit it. And maybe they will, once they get done talking about our great new victory over Iran.